5. November 2020

EU Sugar Market Update

In this article, we will look into developments in the European sugar market since our latest newsletter sent out before the summer kicked in. How did the fundamentals develop and what are the expectations for coming season?

In our latest EU Sugar Market update early June, we were focusing on first consequences to our industry linked to the outbreak of the Corona Virus. It has been clear that the acreage in Europe is further shrinking and a risk had been described that the virus yellow could affect yields.

What has happened since:

Later in the season, there has been plenty of rainfall across Europe during Sep/Oct, which did not support the development of the beets. According to the latest EU MARS report, the EU average yield across all producing member states fell marginally to 72.5 mt/ha, a reduction of 0.7% from September’s report and 2.8% below the 5 year average yields. Countries that had relevant changes to the downside were including relevant ones, like Germany while France remained more or less unchanged at 81.6 tonnes per hectar.

With this unfavorable weather across Europe, the hope of good sugar yields in areas not affected by yellow virus is vanishing. While we were reporting earlier that the mild winter was favorable for aphids but the potential effect was unclear, it indeed now materializes to an extent that is quite significant. France is hardest hit by the virus with 80% of the beet areas south of Paris is infected. North of Paris infection rates are lower but will still have a major impact on the crop. In the UK it is reported that 35% of the beet areas are infected with individual farmers facing yield losses of up to 50%. Beet yield loss across the country are estimated as high as 15% compared to 5-year average. In South of Germany, there are so far only smaller concentrations of the virus but some in some areas of Rhineland-Pfalz and Baden-Württemberg 80%-90% of the fields are affected. It seems that it is only a question of time before the virus will also spread further into the North and the East. A potentially mild winter again would boost the development.

As the outbreak of virus yellow is linked to the ban of neonicotinoids and as it is said that alternative active agents are not yet sufficiently available, the temporarily reintroduction of neonicotinoids usage for beet growers is on the agenda of almost all EU member states. As it looks right now, the French Senate has already approved a neonics derogation and others are in the process to get this done, however unclear when and in what frame this will come. Needless to say, that a level playing field for all producers shall be the aim.

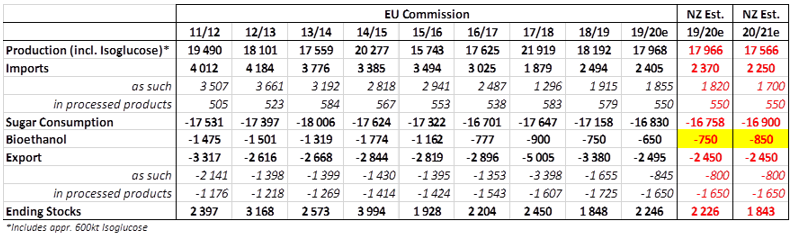

With the above in mind, we have adjusted our sugar production forecast down to 16.8 mill. mt (-2.6% year-on-year) with a further downside risk.

When looking into the EU sugar balance, we have to reflect without a doubt the Corona driven consumption reduction. Seems to be that 300-400 kto in the food industry is a relevant number for the period March 19 until now. On a yearly basis, the number might be up again – especially that the 2nd wave of look downs will again impact the Horeca segment. On another note, we also need to reflect that the import streams of preferential raw and white sugar to Europe are further falling; historical low imports are foreseen for the running sugar marketing year.

Our overall market view therefore remains that the EU sugar market is tight and that despite a hopefully only temporary demand reduction the ending stocks will go further down.