11. Februar 2026

EU Sugar market update

This report reviews recent developments in the European sugar market and provides an outlook following the conclusion of the 2025/2026 beet campaign.

The early onset of winter caused logistical challenges in some regions but did not materially affect what was overall a successful campaign for Nordzucker. Processing ended in December in Finland and Lithuania, followed by Germany and Sweden in late January; the final beets were processed in Denmark, Poland, and Slovakia in early February. Beet diseases and the SBR complex had only localized impacts and did not significantly affect yields or quality.

As part of Nordzucker’s GoGreen programme, further improvements in energy efficiency and CO₂e reduction were achieved through optimized processes, biomethane use from beet pulp, and enhanced steam energy recovery. The company remains on track to meet its 2030 CO₂e reduction targets.

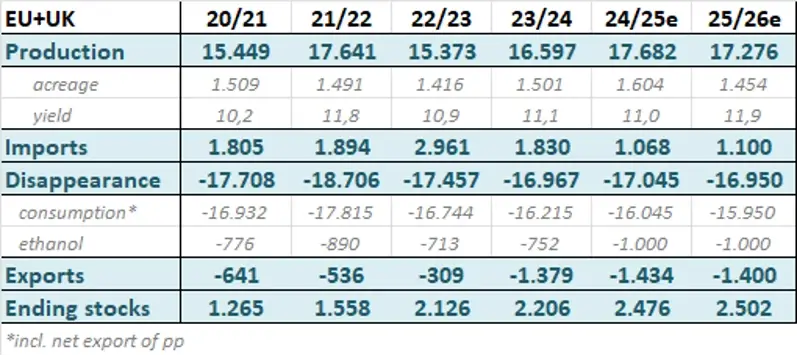

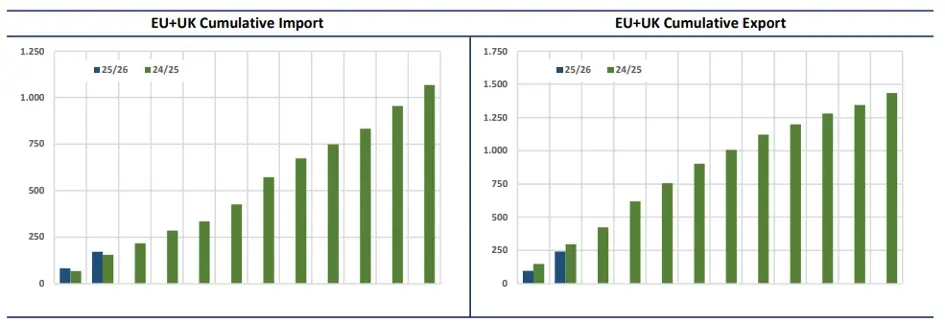

The European sugar sector continues to face structural challenges: declining consumption, low prices, rising stocks, and ongoing consolidation. The 2025/2026 campaign is now largely completed across Europe, with yields revised upward and even reaching record levels in some areas. Despite a 10% reduction in planted area, final EU production is expected to decline by only around 2.5%. Similar trends were seen in Ukraine, Russia, and Serbia, resulting in overall strong production in the Northern Hemisphere.

Since May 2025, global sugar prices have fallen to their lowest levels since 2021. Strong harvests in Brazil, India, and the EU—as well as market uncertainties related to tariffs and currency movements—have increased pressure on EU sugar prices. Additionally, consumption has softened, partly driven by the “chocolate crisis”, further reducing demand.

Looking ahead, the EU sugar market is expected to remain volatile. Prices have recently shown some signs of recovery, supported by expectations of a further reduction in beet area in 2026/2027. A conservative EU‑wide acreage decline of at least 5 per cent, with the potential for deeper cuts can be assumed. Given normal yields, EU sugar production could decrease by around 9% (approx. 1.6 million tonnes). While current stock levels are adequate, it remains unclear whether they will be sufficient under average crop conditions. Over two years, sugar beet area in the whole EU may fall by more than 15 per cent, reaching its lowest level since 2015/2016 and triggering renewed consolidation across the industry.

Nordzucker has already initiated its transformation: due to inconsistent and declining beet volumes in Slovakia, the company will end sugar production at its Trenčianska Teplá factory from 2026 onwards. The site will be developed into a strengthened Commercial & Logistics hub for the domestic and Southeast European markets, supplied primarily from Germany.

Recent reports indicate that the European Commission plans to suspend duty‑free sugar imports under the IPR scheme to support EU producers amid low prices and rising competition. The proposal has generated mixed reactions: beet growers support the suspension, citing market oversupply and a three‑year price low, while the fermentation industry and sugar users attribute the price decline to domestic overproduction and oppose the measure.